Sergey MalchevskiyinDataDrivenInvestorEvent-Based Portfolio Rebalance ApproachToday I’m going to share with you my idea about how to get improved investing performance using machine learning.Feb 4, 20222Feb 4, 20222

Sergey MalchevskiyinTowards Data ScienceFine-Tuning the Strategy Using a Particle Swarm OptimizationHow to define sub-optimal parameters of the trading strategy if the number of the combination is extremely hugeMar 19, 20201Mar 19, 20201

Sergey MalchevskiyinTowards Data ScienceUnsupervised Learning to Market Behavior ForecastingYou will get know how to model the market behavior using Hidden Markov Model. This article includes a trading strategy using this approach.Sep 10, 20197Sep 10, 20197

Sergey MalchevskiyinTowards Data ScienceApplication of Gradient Boosting in Order Book ModelingCreating an ML model that forecasts the price movement in the order book. This article contains a full-cycle of research.Jun 18, 20193Jun 18, 20193

Sergey MalchevskiyinTowards Data ScienceBayesian Optimization in TradingToday, I’m going to show how to apply Bayesian optimization to tuning trading strategy hyperparameters.Feb 15, 2019Feb 15, 2019

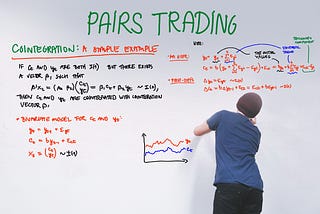

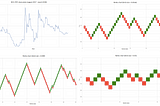

Sergey MalchevskiyinTowards Data SciencePairs Trading with CryptocurrenciesSubscribe to our Telegram channel for more insights into the world of trading.”Dec 5, 201810Dec 5, 201810

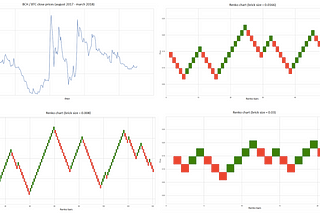

Sergey MalchevskiyAdaptive Trend Following Trading Strategy based on RenkoAlgorithmic trading strategy based on Renko brick size optimization approach. The article contains: concept, algorithm, code, backtesting.Nov 19, 20184Nov 19, 20184

Sergey MalchevskiyHow to Develop a Stock Market Analytical Tool using Shiny and RSubscribe to our Telegram channel for more insights into the world of trading.”Apr 17, 20187Apr 17, 20187

Sergey MalchevskiyinTowards Data ScienceRenko Brick Size OptimizationSubscribe to our Telegram channel for more insights into the world of trading.”Mar 31, 201810Mar 31, 201810